Over the weekend I got together with some buddies to watch the UEFA Champion’s League Soccer Finals at the Loose Goose in Walkerville.

Great spot to watch a game, by the way!

I brought along my 5-year-old son, Ben, with me.

I wasn’t sure what to expect… I honestly didn’t think he would last past the first half.

Much to my surprise, he lasted the whole game.

And seemed to enjoy himself.

It probably didn’t hurt that the bartender kept topping off his apple juice…

We’re leading into a big month of soccer… Euro Cup and Coppa America!

Forza Italia and Let’s Go Canada!

Stay tuned for future updates! lol

Okay, so as I’m sure most have already heard, the Bank of Canada cut the overnight interest rate yesterday, by 25 bps.

Finally!

And it’s not just the real estate community that is thrilled about the news… Everybody and their mother seem to be celebrating this announcement.

In and of itself, aside from providing a bit of relief to variable rate borrowers, a 25-point cut doesn’t move the needle a whole lot…

But I believe what is being celebrated here is the relief that we have successfully transitioned from a rate increase cycle to a rate hold period, to what will likely now be a rate cut cycle.

The question becomes… how many cuts, and how fast…?

But before we break out the champagne…

As I’ve said before… be careful what you wish for…

Rate cuts don’t mean that things in the economy are better…

It means things likely aren’t good… and it is probably a signal that the Bank of Canada thinks they might get worse.

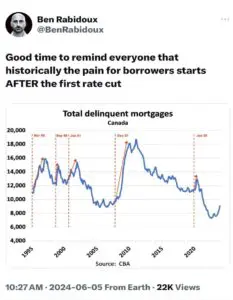

As the chart above shows… historically, after a rate cut, you start seeing more mortgage defaults.

This is probably because the Bank of Canada has access to information, we don’t have…

and they probably have a good idea of what’s to come… and are trying to get ahead of it by starting to cut rates.

Switching gears, and moving on from one politician to another…

Have you heard the recent comments made by PM Trudeau?

In a recent interview with The Globe and Mail’s City Space podcast, our Prime Minister commented that “Housing needs to retain its value. It’s a huge part of people’s potential for retirement and future nest egg.”

These are very bold comments considering the growing generational wealth divide and the current housing crisis.

Maybe this was a good ol’ Freudian slip by the PM, or perhaps his comments were intentional and an indication of who he believes his target voter base is in the next election — baby boomers/homeowners.

Regardless of the motivations behind the comments… he’s telling the truth.

Asset prices can’t go down. And that includes housing assets.

It sounds a lot nicer to say that housing prices can’t go down because we need to protect the retirement plans of good, hard-working Canadians.

But that’s not the real reason.

Our financial system is designed to inflate.

And that inflation makes its way into asset prices. Real estate is just a benefactor of that.

Because we are a debt-based system, there needs to be more and more dollars in the system to pay for the debt.

More dollars lead to greater asset prices.

Greater asset prices make the increased debt not look as bad.

The focus for the last couple of years has been to tame inflation… but that’s a bit misleading.

The system needs and wants controlled inflation… but the recent pace of inflation just got out of hand because of all of the covid era policies.

The real enemy though, is deflation.

The biggest risk to our financial system is asset prices going down in value.

Just think about the banks… a key participant in Canada’s economy. What will happen to all those mortgages if the underlying assets start to go down in value?

So it’s not really just about houses…

It’s about assets in general.

And in a debt based system (which is what we have)… for the system to work, asset prices need to go up in a controlled manner, and you need to have more and more dollars in the system to provide liquidity to pay for those assets.

I’m not saying that housing prices never go down… or that they will go up in a straight line…

but what I am saying, is that long periods of significant declining prices are very unlikely.

And it sounds to me like the PM agrees with me… lol

Okay, that’s it for this week.

Fee free to reach out to discuss if the most recent rate cut has any impact on your financial situation.

Until next time,

Vince