Several years ago (before the pandemic), I attended a real estate/investor event put on by a group called Rock Star Real Estate. They are two brothers who own a real estate brokerage located in Oakville, Ontario, focusing on helping investors purchase rental properties.

They’ve built an amazing real estate brokerage and have helped hundreds of clients acquire attractive investment properties.

During the event, they shared how concerned they were that their kids would never be able to buy a home.

Home prices in the Greater Toronto Area had been escalating much faster than average incomes and many families were priced out of the housing market.

On my drive home, I can still remember thinking about how lucky we were in Windsor-Essex because homes were still affordable in many areas.

Well, fast forward to today and everything has changed drastically.

Our kids are now in the exact same situation and sadly, they may never be able to buy a home as the cost of home ownership has skyrocketed.

If you have children and they don’t yet own a home, without help from mom and dad, there’s a chance that they’ll never be able to buy one.

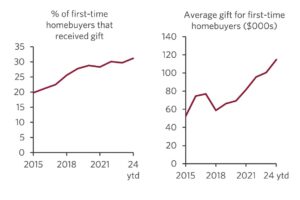

A recent CIBC report found that nearly a third (31%) of first-time buyers needed a gift (usually from their parents) to help buy a home in the bank’s 2024 YTD data. That’s up from 20% back in 2015, which seemed high back then.

Source: CIBC

The amount of money gifted has also seen a sharp increase. The average gift this year was a whopping $115,000, up 73% since 2019 — right before the interest rate cuts. One would expect the amount of the gift to increase, but the amount as well as the share of buyers requiring parental help. That’s a compounding problem that becomes much harder to fix.

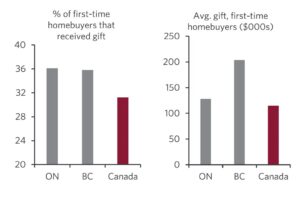

First-time buyers in Ontario require even wealthier parents.

The share that used a gift was roughly 36% in Ontario, 5-points higher than national data. The average gift’s dollar value was also significantly more expensive in Ontario ($128k).

“Homebuyers relying on a wealth transfer from their parents in order to purchase a home is becoming the norm in Canada,” explained Benjamin Tal, deputy chief economist at CIBC World Markets, and the co-author of the report.

He adds, “this phenomenon is helping to mitigate the bite of housing inflation for buyers, but unfortunately it is also contributing to a widening of the already wide wealth gap in Canada.”

This is a very sad situation.

The average young adult is now in a very challenging financial situation that will end up negatively impacting the rest of their lives, as they won’t be able to accumulate any real assets.

They won’t be able to buy a home, and they won’t be able to save for their future retirement.

The cost of living has escalated to the point where most young adults are now living paycheque to paycheque.

And if they’re unable to acquire any real assets, they WILL end up struggling financially for their entire lives.

To stop this scenario from playing out in their lives, they must start educating themselves NOW.

And the sooner they can start accumulating assets, the better!

Please understand that I’m not sharing all of this as clickbait. I’m sharing it because it’s a distinct possibility for them.

Having three young kids myself, this is something that is always in the back of my mind.

Recently, we put together a Guide, to help prospective first-time home buyers in Ontario, purchase their first home.

By no means is this guide the solution to this much bigger problem.

But it will provide a good head start in the journey toward purchasing a first home.

And the quicker you can get there the better… because I don’t see housing affordability getting better anytime soon.

If you or anybody you know is looking to purchase their first home, then download this guide.

Or if you ever want to go deeper into this stuff, please reach out!

I would be more than happy to buy you an espresso and talk finances.

Until next time,

Vince