This is a picture of my wife, Jackie, and oldest daughter, Emma, riding the Drop Tower, at the LaSalle Strawberry Fest, this past weekend.

As long-time La Salle residents, we love the Strawberry Fest.

Jackie and I would go with our parents when we were kids, and with friends as we got older.

Now we’re taking our kids to the Strawberry Fest.

And if I had to guess, it won’t be long before our kids ditch Mom and Dad and ask to go with their friends… sigh.

But until then, it’s an annual tradition that we will continue.

Jackie is a trooper… she goes on every ride with the kids.

I did my fair share of rides as well this year… but zero chance I was going on the Drop Tower.

That drop is way too much for my stomach to handle.

Speaking of drops… did you hear that Bank of Canada cut rates by 25 bps!?

Of course you did… every realtor and mortgage agent in Canada is posting about it.

But what’s the real impact of 25 bps rate drop??

First off, it mainly only affects variable-rate borrowers.

And what is the affect?

Assume you are a variable rate borrower… for every $100,000 you borrow; a 25 bps decrease will reduce your payment by $15/month.

I’m not sure this is enough to really move the needle.

Even for a highly leveraged real estate developer… A 25 bps reduction is not game-changing. It won’t change the financial equation for them.

And the reality is that variable-rate borrowers are a small portion of the market.

The vast majority of home buyers are still taking fixed-rate mortgages, and fixed rate mortgages haven’t really changed all the much over the last 6-12 months.

That’s because fixed rates are governed by the Bond Market…

And when the Bank of Canada reduces its prescribed rate, this does not have any direct impact on the bond market.

So the most recent 25bps rate cut has very little impact on the overall market.

One of the Bank of Montreal Economists agrees with me on this…

“Most market participants have been eagerly awaiting this cut, and there will surely be a psychological boost now that the peak of this rate cycle has most likely been set,” explains Robert Kavcic, senior economist at BMO.

Adding, “But at the same time, a 25 bp trim to variable rates from 23-year highs is very little actual relief when most borrowers have already moved to lower fixed-rate mortgages.”

“The overnight rate only directly impacts variable-rate mortgage costs. Fixed-rate mortgages move with bonds of similar terms, and they’re already much cheaper. He notes that fixed-rate mortgage interest delivers about 125 basis points (bps) of value. Buyers are already making use of the cheaper credit.”

BMO also points to regulatory data showing that the majority of new lending is fixed-rate loans, especially 5-year terms. In contrast, they found just 10% of new loans over the past 12 months have been variable-rate loans.

“…if the market is mostly operating on fixed rates right now, this week’s move doesn’t alter the calculus much even if it does provide a psychological boost,” explains Kavcic.

So obviously more rate cuts are needed…

But how many will get?

Or a better way to ask the question, is how many rate cuts CAN we get?

To a certain extent, we are restricted by what the U.S. Federal Reserve does.

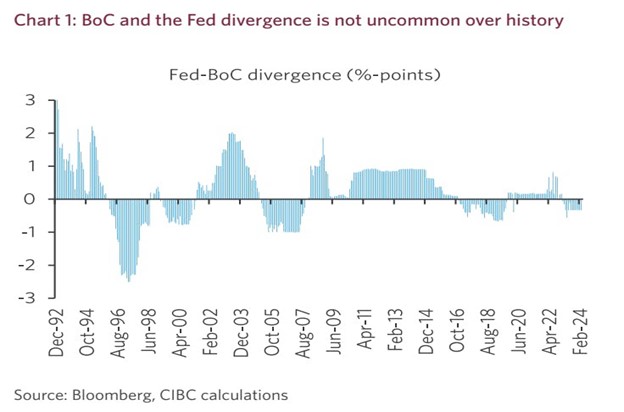

Check out this chart by CIBC…

It shows how far our rates diverge from the ones south of the border since 1992.

Over the last 20 years, the maximum difference in rates has been 1%.

With this latest cut in Canada the difference is about 0.5%.

Can they drop them much more without the U.S. doing the same?

Bank of Canada Governor, Tiff Macklem, even addressed this in his most recent press conference.

I interpreted his banker talk as he is okay with sacrificing the Canadian dollar slightly, but he will be very careful with this balancing act… (i.e. very careful with how quickly and how much they cut rates in comparison to the Federal Reserve).

So what it all boils down to is that traditionally, a rate cut should help to boost demand — or at least remove some of the friction.

But that might not be the case this time around, since affordability is stretched to the point that the rate cut will have little impact.

So further rate cuts are needed, but is it even possible to cut as much as might be required??

Let’s see how this plays out.

Until next time,

Vince